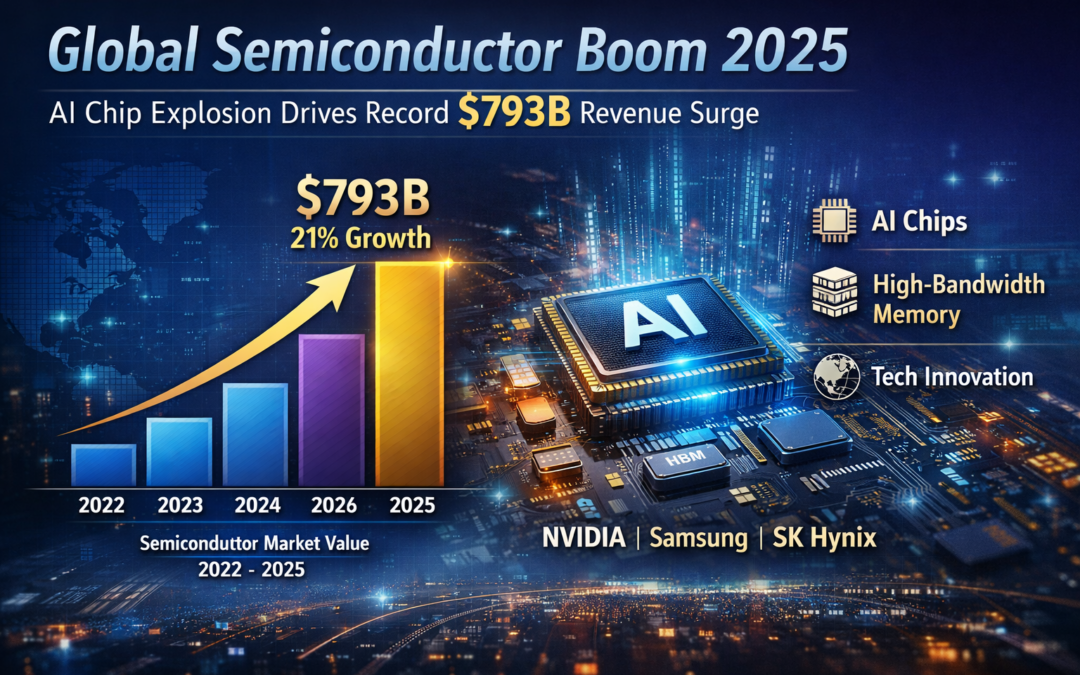

Worldwide semiconductor revenue surged to a record $793 billion in 2025, delivering 21% year-over-year growth, according to Gartner, as AI infrastructure spending reshaped global technology markets. The acceleration reflects a structural shift where AI compute, memory, and advanced packaging increasingly define both financial performance and long-term semiconductor strategy.

- Worldwide semiconductor revenue reached a historic $793 billion in 2025, delivering 21% year-over-year growth and confirming semiconductors as a primary driver of global technology expansion. AI infrastructure investment emerged as the dominant catalyst behind this acceleration.

- AI-focused semiconductors — including GPUs, AI accelerators, networking chips, and high-bandwidth memory — generated nearly one-third of total industry revenue, signaling a decisive shift toward compute-intensive workloads. Enterprise AI adoption continues to reshape silicon design priorities and capital allocation.

- NVIDIA surpassed $100 billion in annual semiconductor revenue, widening its lead over competitors and redefining scale economics in the AI chip market. GPU-centric platforms now anchor hyperscaler, cloud, and sovereign AI strategies worldwide.

- Samsung Electronics maintained the second-largest semiconductor revenue position, supported by memory market recovery and AI-driven demand for advanced DRAM. Memory pricing discipline and AI-optimized products strengthened margin resilience despite softness in non-memory segments.

- SK Hynix advanced to third place globally, fueled by explosive growth in high-bandwidth memory (HBM) shipments. Specialization in AI-critical memory solutions accelerated revenue share gains and long-term strategic relevance.

- Intel experienced relative revenue pressure as market demand shifted toward AI-optimized architectures and accelerators. Competitive dynamics increasingly favor heterogeneous compute, specialized silicon, and ecosystem-driven platforms.

- High-bandwidth memory accounted for approximately 23% of total DRAM revenue in 2025, exceeding $30 billion in annual sales. AI training and inference workloads continue to elevate memory bandwidth as a core performance constraint.

- AI processors alone generated more than $200 billion in semiconductor revenue, positioning AI compute as the industry’s fastest-growing and most capital-intensive segment. R&D investment cycles are now tightly aligned with AI roadmap execution.

- Semiconductor industry growth at this scale is accelerating fab investments, advanced packaging adoption, supply-chain localization, and ecosystem consolidation, reshaping competitive positioning across design, manufacturing, and OSAT services.

- Sustained semiconductor expansion is driving employment growth across Asia-Pacific, particularly in advanced manufacturing, IC design, packaging engineering, and technical leadership roles. Talent demand is rising fastest in AI-centric semiconductor hubs across East and Southeast Asia.

Need efficient semiconductor packaging or top executive and technical talent?

We deliver high-quality carrier tapes, cover tapes, reels, and thermoforming trays tailored for the industry’s most in-demand and advanced packages: from PDIP, SOIC, and QFNs to WLCSP, chiplets, modules, and panels.

At the same time, we connect you with the best-fit Senior Management leaders, Professionals, and Technical Staff to strengthen your organisation.

For enquiries or more information, please visit our website: https://tmbsconsulting.com or Contact Richard Chuck Olivas via WA: https://wa.me/+6583393490

#SemiconductorIndustry #AIInnovation #HighBandwidthMemory #ChipManufacturing #AdvancedPackaging #NVIDIA #Samsung #SKHynix #Intel #GlobalTechnology